Transatlantic Investment Protections: Convergence or Sticking Point for the TTIP?

Greg Anderson

University of Alberta (CANADA)

Dr. Greg Anderson was a DAAD/AICGS Research Fellow in March and April 2017. He is currently Associate Professor in the Department of Political Science at the University of Alberta (CANADA) and former Research Director (2009-2013) of the Alberta Institute of American Studies (AIAS) at the University of Alberta. He earned a BA and MA in American History at Brigham Young University and the University of Alberta, respectively, and completed his PhD in 2005 at the Paul H. Nitze School of Advanced International Studies of the Johns Hopkins University (Johns Hopkins/SAIS) in Washington, DC. During his time in Washington, he served as Policy Analyst (2000-2002) for the Western Hemisphere Office of the United States Trade Representative (USTR) under both President Bill Clinton and George W. Bush.

Dr. Anderson’s research has been funded by the Social Sciences and Humanities Research Council of Canada (SSHRC) and the U.S. and Canadian-based Donner Foundation. His teaching interests are broadly situated within the discipline of international political economy, particularly the political economy of North American integration. He has authored numerous pieces focused on Canada-U.S. relations, the politics of international trade and investment policy, U.S. foreign economic policy, and the impact of the global economy on forms of governance in venues such as The World Economy, the Journal of World Trade, and Diplomatic History. Greg’s recent writing has included a focus on the contemporary debate over foreign direct investment rules and the experience with investor-state dispute settlement (ISDS) within the NAFTA area. Dr. Anderson is also the co-editor (along with Dr. Chris Kukucha) of International Political Economy (Toronto: Oxford University Press, 2016). He regularly provides expert commentary for major Canadian radio, television, and print media outlets.

As a DAAD/AICGS Fellow in the Spring of 2017, Dr. Anderson will be advancing his research and writing on foreign direct investment rules and the controversies that have swirled around the U.S. and European experiences with them. More narrowly, Dr. Anderson’s project will focus on how those rules might have evolved in the proposed Transatlantic Trade and Investment Partnership (TTIP) and where they may now be headed in an era of anti-global populism on both sides of the Atlantic.

This paper is about the controversy swirling around foreign direct investment rules generally, and recent U.S. and European experiences in helping reshape their design. When this research project was proposed in mid-2016, its purpose was to look ahead at how investment protection rules had evolved on both sides of the Atlantic as a window into how investment rules might have evolved in the proposed Transatlantic Trade and Investment Partnership (TTIP).

The conclusions and point of this paper are that the United States and Europe were on a path toward convergence on investment rules that would have made them less contentious within the TTIP negotiations than many assumed. It’s a conclusion that remains valid, but contingent on what becomes of TTIP as the effects of Brexit and the election of Donald Trump in 2016 unfold.

The antecedents of contemporary investment rules—bilateral investment treaties (BITs)—have been around for decades and generated virtually no controversy. Yet, in 2009 and again in 2012, the Swedish power company Vattenfall pursued investment arbitration against Germany under the terms of the Energy Charter Treaty alleging the expropriation of property as a result of Berlin’s decision to, in the first instance, phase out certain coal fired power generation (Vattenfall I), and, in the second, shutter its nuclear power generation in the wake of Japan’s Fukushima nuclear disaster (Vattenfall II).

The Vattenfall cases hijacked the EU’s nearly completed free trade negotiations with Canada, forcing a re-think by Brussels most have assumed would complicate TTIP talks with the United States.

BITs, BITs, and More BITs

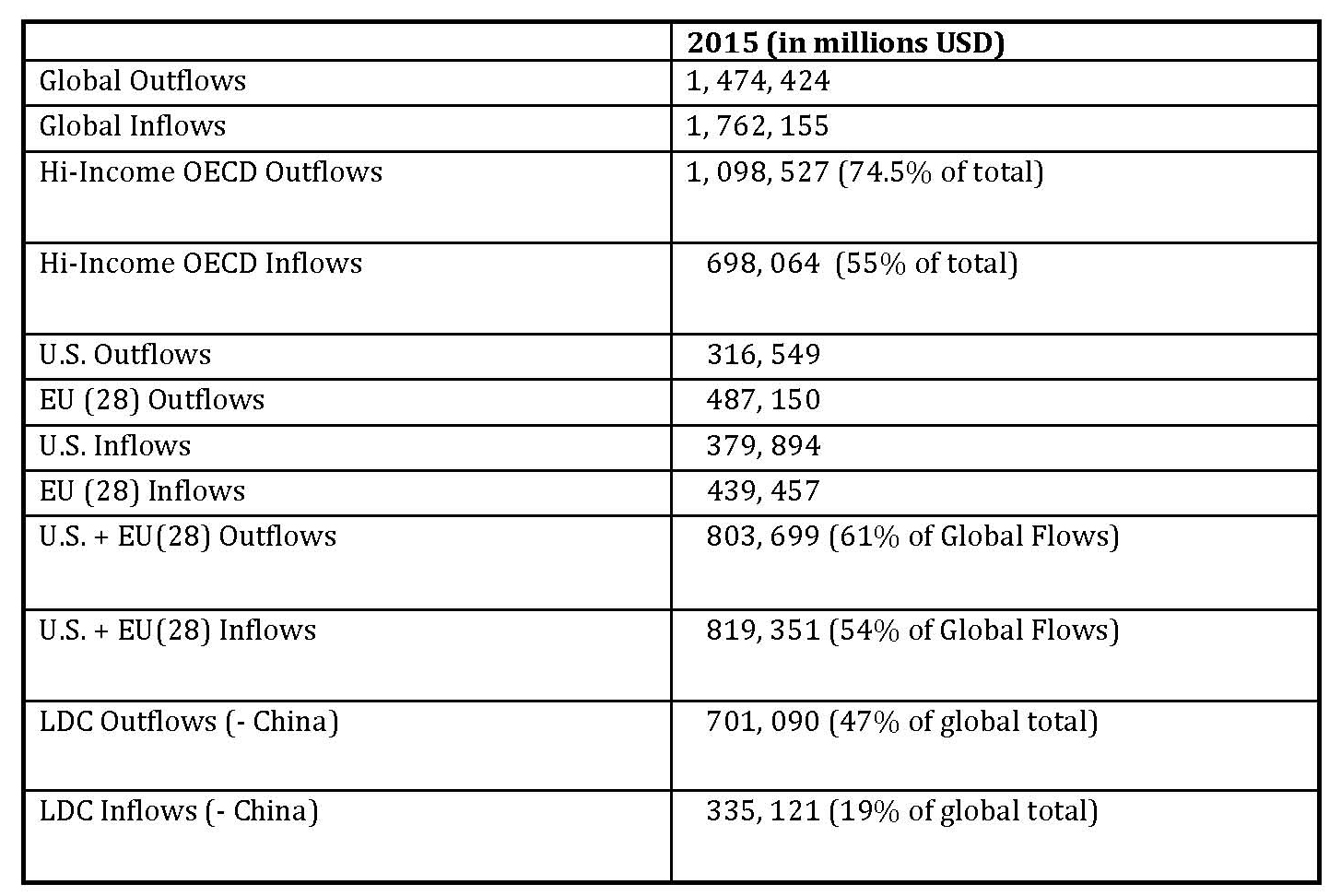

Although foreign direct investment (FDI) is widely viewed as an important potential source of economic development, very little FDI flows toward the developing world. According to the United Nations, in 2015 there were nearly $3 trillion worth of foreign direct investment flows globally. Unfortunately, the lion’s share of those flows are between wealthy OECD countries, accounting for more than 70 percent of all outflows and more than 50 percent of all inflows (see Table 1).

Table 1: Global Flows and U.S., EU Shares

Moreover, if we take away the large flows into and out of China, investment flows into the developing world represent a paltry 19 percent of all global inflows. The reasons for this discrepancy are multifold and include things such as poor infrastructure, the lack of market proximity, or access to a skilled labor force.

However, one of the most important historical challenges concerns the rule of law, or lack thereof. A major hole in international law historically has been the lack of “standing” or “personality” for private actors. The challenge for private actors contemplating the commitment of investment capital in parts of the developing world is simple; the potential for discriminatory treatment, including expropriation, by host governments. Private actors can complain to home-country governments about their treatment abroad, but the sovereign state remains paramount.[1]

Since the late 1950s, states sought to fill this legal vacuum through the use of bilateral investment treaties (BITs) setting the legal terms under which private capital flows will be treated by host nations.[2] According to UNCTAD, there are currently nearly 3,000 BITs and more than 350 other treaties with investment provisions, the very first of which was the Germany-Pakistan BIT in 1959.

1994 Was a Very Big Year

Germany and the United States have more than 300 BITs between them and developing countries, none of which generated any controversy.[3] However, in 1994, both the North American Free Trade Agreement (NAFTA) and the Energy Charter Treaty essentially had BITs inserted into them.

Soon after U.S. BIT Model language was inserted into the NAFTA, effectively creating the world’s first trilateral BIT, Chapter 11 began generating unintended consequences. The NAFTA negotiators assumed that Mexico, with its twentieth century history of expropriation, was the natural target of investment rules and that the so-called investor-state dispute settlement (ISDS) provisions would, if invoked at all, likely be deployed as a defense against discriminatory treatment by Mexico. Starting in 1997 with Metalclad’s claim that Mexico failed to live up to its contractual obligations over the firm’s investment in a hazardous waste project, it appeared the NAFTA was working as intended.

However, that same year, The Loewen Group, a Canadian funeral services firm, challenged an adverse Mississippi court ruling under the terms of NAFTA Chapter 11, significantly altering the political dynamics of investment protection rules. Never before had such rules been used by a firm from a developed country to challenge treatment of an investment in another developed country.

To date, there have been fifty Chapter 11 cases alleging discriminatory treatment at the hands of a NAFTA government, only fourteen of which have been filed against Mexico. The rest, eighteen each, have been against Canada and the United States. The distribution and substance of Chapter 11 cases have fueled criticism that investment rules were being used to undermine (not enhance) the rule of law by giving firms a pathway for challenging the state’s sovereign power to regulate through a legal process unavailable to domestic firms. That perception was compounded in late 1999 when Methanex Corp., a Canadian petrochemical firm, challenged a California regulation banning a fuel additive proven to be toxic to groundwater supplies.

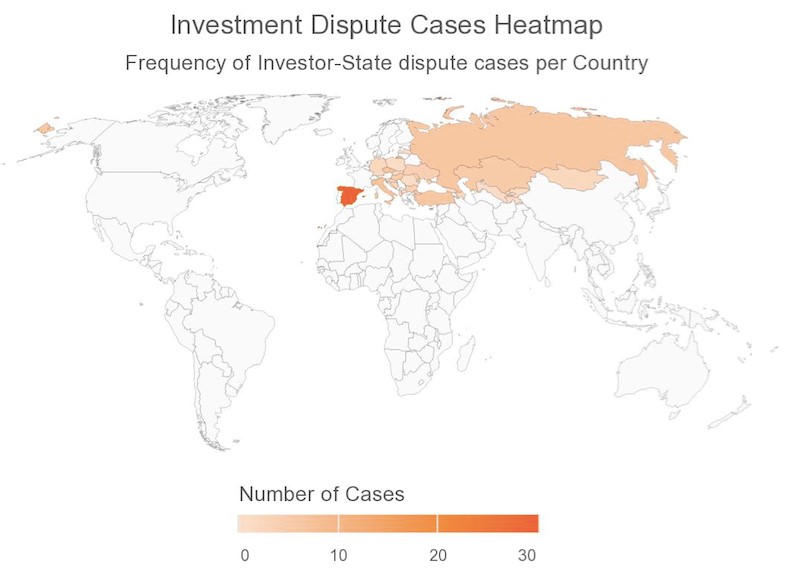

Across the Atlantic, the European Energy Charter was expanded, renamed the Energy Charter Treaty in late 1994 and, like the NAFTA, infused with ISDS provisions. Much as Mexico was the assumed target of investment protections in the NAFTA, it was those with checkered histories of property rights protections—such as Russia or former Soviet republics—who were assumed to be the likely defendants in Energy Charter cases. And, as the charts below depict, that’s how they initially unfolded.

Yet, in recent years, Energy Charter Treaty ISDS cases have spiked, and increasingly included measures in ostensibly developed countries with stable histories of property rights. A case in point is Spain, which had sixteen new filings in 2015 alone arising from reduced domestic subsidies to the renewable energy sector—the state allegedly moved the regulatory goal posts.

Table 2: International Energy Charter Case Distribution

An ISDS Earthquake and Tsunami in Germany

The political consequences of the Vattenfall cases could not have been worse for Europe’s negotiations with Canada (CETA), and forced the EU into a hasty reconsideration of its position on ISDS.

European civil society’s objections to the CETA included typically controversial issues such as agriculture, intellectual property, and culture, but ISDS became a lightning rod of controversy capable of drawing tens of thousands of protesters into the streets of European cities.

The CETA was always something a test-bed for the much bigger TTIP talks with the Americans (formally launched in 2013), but the controversy over investment with Canada forced the EU’s hand on making its position on ISDS more concrete.

The Big Investment Fish

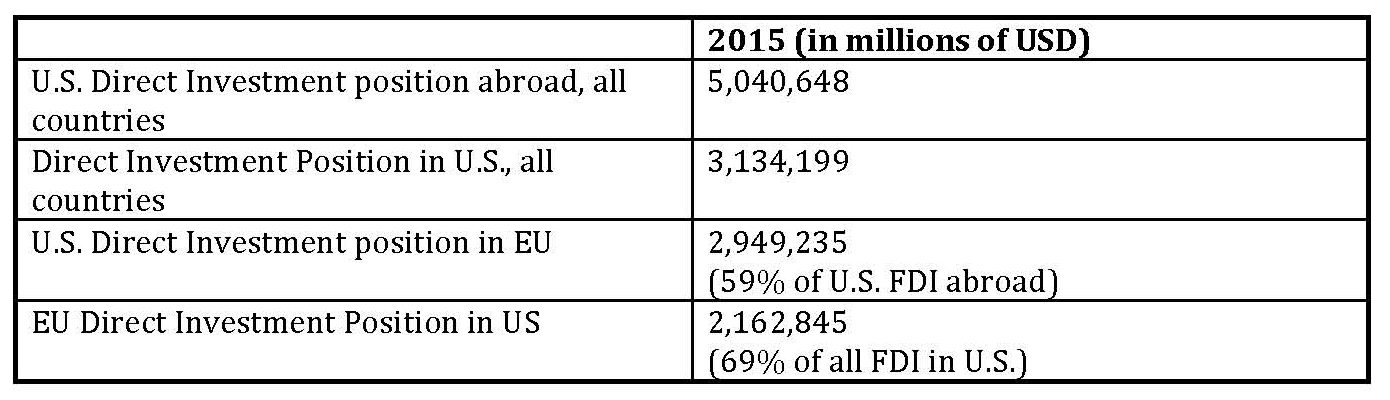

As noted above, global investment flows have overwhelmingly been between advanced industrial countries (see Table I), and the lion’s share of that has flowed between the United States and Europe. Moreover, large stocks of existing U.S. and European investment are already present in each other’s jurisdictions. As depicted in Table II, in 2015 nearly 60 percent of all U.S. investment abroad was located in Europe and nearly 70 percent of all overseas European investment was located in the U.S.

Table 3: U.S.-EU FDI Flows

With such large volumes of investment across the Atlantic, formalizing investment protection rules has, to some, seemed an obvious goal. In 1995, the members of the Organization for Economic Cooperation and Development (OECD), began talks aimed at concluding a multilateral set of investment rules known as the Multilateral Agreement on Investment (MAI). By early 1998, the talks had collapsed in spectacular fashion. Civil society, alarmed by the early experience with the NAFTA, breathed a sigh of relief and declared victory. The OECD membership, on the other hand, was deeply divided over what the terms of those rules ought to be.[4]

Transatlantic Shock and Awe

Parallels in the North American and European experiences with ISDS go beyond their insertion in the NAFTA and Energy Charter Treaty in 1994.

One reason BITs generated so little controversy in the United States and Europe is that FDI tends to flow mostly in one direction; from rich to poor countries. There simply isn’t a lot of developing country capital flowing into developed countries over which a dispute could be filed.

Large flows of FDI between developed states suggest a much stronger potential for disputes. Negotiators for both the NAFTA and Energy Charter Treaty should have seen this coming. They did not. Governments were taken aback by the incidence of disputes against states with strong property rights protections.

Parallels also exist in the responses of the United States and Europe to these challenges.

In the United States, the 1999 Methanex case under Chapter 11 of the NAFTA rattled nerves inside and outside government. Methanex prompted NAFTA governments to intervene that summer with a ministerial “interpretation” of the meaning of parts of Chapter 11.[5] Yet, as worrisome NAFTA cases advanced, the Department of State launched a review of the U.S. BIT program in 2004, the first revision of the U.S. BIT Model since it was inserted into the NAFTA in 1994. The 2004 BIT Model formed the template for subsequent U.S. trade and investment agreements until 2009 when yet another revision exercise made further changes, resulting in the 2012 Model BIT.

In Europe, the furor arising from the Vattenfall cases prompted German officials to press the Commission for changes to how the EU pursued investment. In March 2014, German officials signaled that the CETA negotiations could be imperiled without significant changes to the investment chapter. Largely at the behest of Germany, the Commission surveyed member state governments via the Council of the European Union (government ministers) about whether ISDS should even be a part of future European trade agreements. Hearing that the answer was “yes,” the Commission initiated an online public comment period seeking views on changes to future investment chapters.

A number of those suggestions were inserted at the eleventh hour as a way to save the CETA from being rejected. More importantly, many of those comments made their way into EU proposals on investment to be tabled in the context of the TTIP negotiations with the United States.

What follows is a side-by-side comparison of recent reforms to ISDS on each side of the Atlantic. They are reforms borne of near-misses, controversies, and surprises with ISDS provisions as crafted in 1994, but hitherto never applied to developed country groupings with significant levels of cross-border investment.

Models of Convergence?

EU Investment Proposal 2015/CETA vs. U.S. BIT Model 2012

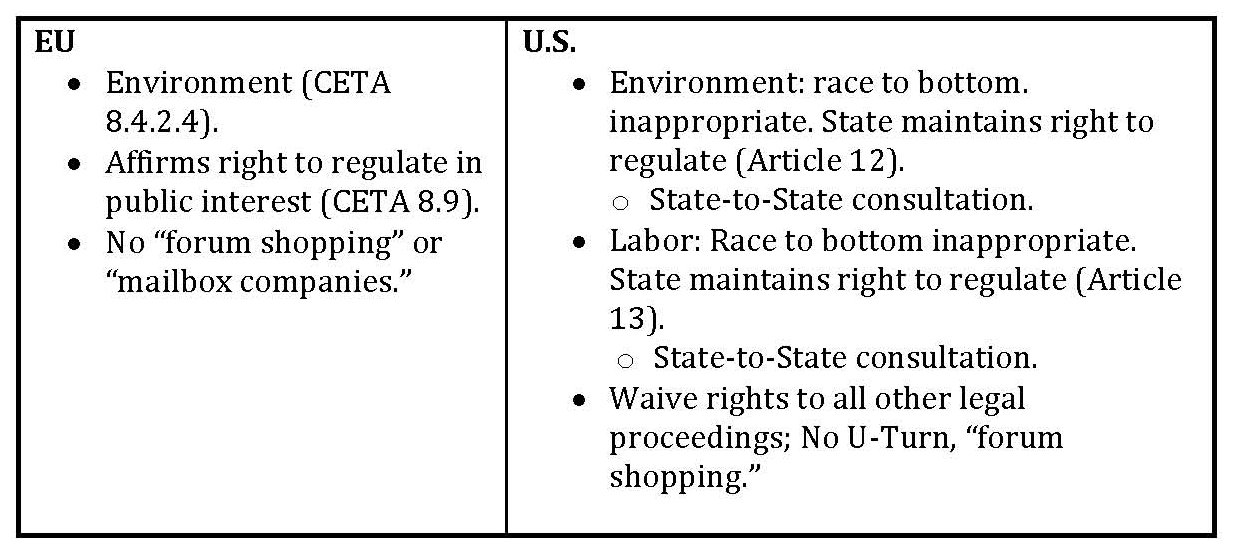

Right to Regulate

Perhaps the most potent public critiques of ISDS provisions is that they afford foreign investors a set of mechanisms for challenging the state’s regulatory power. Moreover, because those mechanisms are unavailable to domestic firms, critics also allege ISDS creates an unconstitutional legal forum with no domestic judicial review. Indeed, in both the NAFTA and Energy Charter Treaty contexts, private firms have alleged regulatory measures adversely affecting revenue streams amount to forms of expropriation.

Reforms have strongly affirmed the state’s right to regulate in the public interest. Moreover, that power is explicitly upheld where labor and environmental regulation is concerned—State Parties may not weaken labor or environmental laws to incentivize FDI flows. Moreover, reforms now severely limit the capacity to abuse ISDS provisions as part of “forum shopping” or the establishment of “mailbox companies” to seek damages.

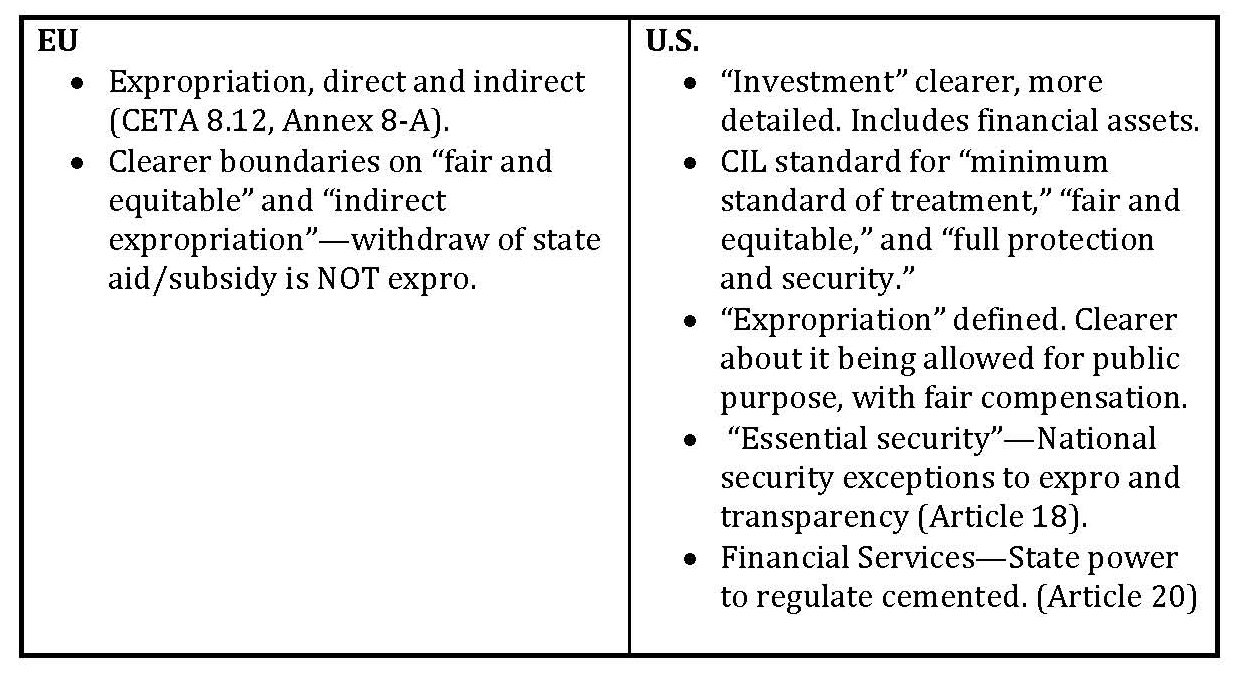

Definitions

Another important area for reform of investment rules is simply definitional. In the NAFTA context, firms began exploiting an absence of definitive language over what an “investment” actually was, what were “fair and equitable” or “minimum standards” or treatment, what was the state’s obligation to provide “full protection and security,” and, of course, “expropriation” itself. NAFTA Chapter 11 was just twenty-two pages long, the 2012 BIT Model is over forty, in part, because of far more attention paid to definitions in an effort to limit the use of ISDS to all but clear-cut violations of property rights. Europe has also moved in the direction of definitional clarity setting out much clearer boundaries on many of the same issues.

Transparency

ISDS

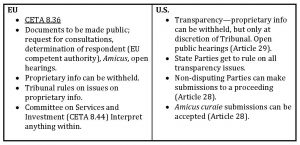

One of the most basic critiques of ISDS has been the lack of transparency. One of the challenges here has been the sensitivity of proprietary information held by private litigants; in short, open arbitration proceedings would expose proprietary information to competing firms. However, the absence of public scrutiny over a process used to challenge state measures has become politically untenable. On both sides of the Atlantic, access to ISDS proceedings through amicus submissions, public hearings, publication of government pleadings, and a much stronger preference for releasing even proprietary information to the public are helping to improve the perceived legitimacy of ISDS.

Advocates on both sides of the Atlantic have argued ISDS should be scrapped entirely. After all, they argue, why do you need an arbitration mechanism for investments in developed country jurisdictions with virtually no history of nationalization or expropriation for reasons other than the public interest? Hence, it is curious that EU member states were unanimous in their support for including ISDS in future EU trade negotiations.

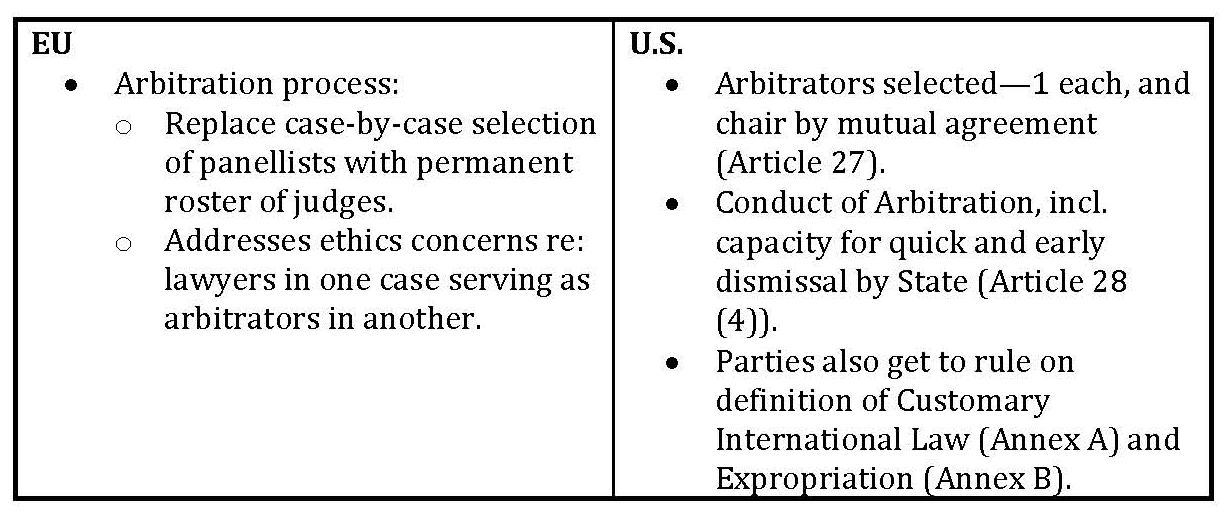

The major difference remaining between the U.S. and EU in ISDS is with respect to the process by which arbitration proceedings are populated with jurists. The United States continues to favor an ad hoc process of selection of panelists, none of whom need be lawyers, whereas Europe would like to establish a permanent roster of possible panelists comprised entirely of judges. Proponents of the U.S. approach argue the character of investments may necessitate sector-specific, rather than purely legal, expertise. Moreover, they argue, an ad hoc system is no more susceptible to ethics problems than the permanent roster of judges proposed by the EU.

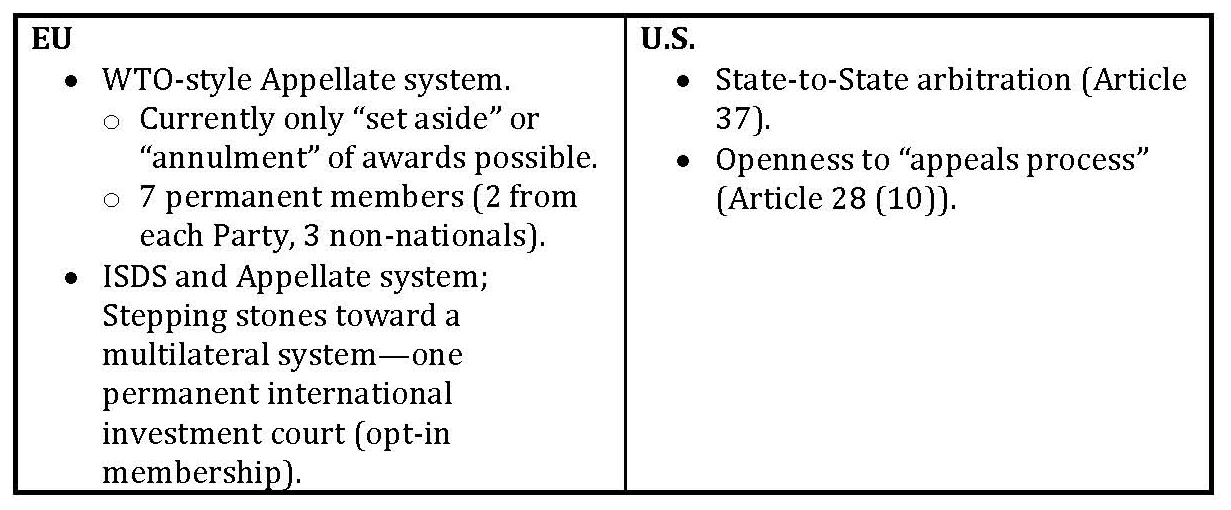

Institutions

Both the EU and U.S. have put the idea of some kind of “appellate system” on the table for future investment chapters, the EU proposal going furthest in suggesting it be modeled on the WTO’s appellate mechanism. Historical skepticism about such institutions in the U.S., particularly some Congressional factions, might make this difficult no matter how it’s designed. However, the U.S. hand in first designing and using the WTO’s appellate mechanism suggests an appeals process for ISDS cases is possible. Moreover, an appeals process would directly address one of the most pointed critiques of ISDS: that proceedings are both secretive and lack oversight.

Yet, it is over the EU’s proposals for an “international investment court” that the biggest divisions with the U.S. could develop. The traditional U.S. aversion to binding institutions is usually strongest in instances where pooled sovereignty is proposed. The EU’s proposal calls for a multilateral court and roster of judges to rule on investment disputes between member states and their private sector investors, and raises a set of long-standing issues that, in part, contributed to the failure of the MAI in 1998.

The substantive differences between the EU proposal and existing multilateral mechanisms for investment (ICSID and UNCITRAL) is unclear. It’s also unclear whether the EU’s proposal is designed to supplant those institutions, or work in conjunction with them. Both ICSID and UNCITRAL and have long track records of facilitating the resolution of investment disputes, including those launched under the NAFTA and Energy Charter Treaty.

Conclusions

In the context of the contemporary populism roiling global politics, no trade liberalization agreement, particularly one as large as the proposed TTIP, is going to be straightforward.

However, this analysis highlights that the respective experiences with investment protections in the United States and Europe have paralleled one another in many ways, starting with the insertion of previously innocuous, uncontroversial BIT-like provisions into the terms of the NAFTA and Energy Charter Treaty in 1994. In both instances, and for the first time, formal investment protections were being applied to developed country jurisdictions into and out of which there were substantial flows of FDI. Controversy ensued as foreign firms creatively availed themselves of ISDS mechanisms, exploited linguistic vagaries, and seemingly challenged the state’s power to regulate in the public interest. A decade later, the terms of the Energy Charter Treaty generated a similarly surprising set of cases.

In both the United States and Europe, the apparent shortcomings of early 1990s investment models prompted reforms over the same issues on both sides of the Atlantic. In both cases, the reforms maintain the utility of investment protections, but recalibrate the state’s relationship to the private firms in the context of robust flows of FDI.

Finally, this paper argued that the respective experiences of the United States and Europe with respect to investment was driving them toward a convergence of views, particularly on issues of transparency and assertion of sovereign regulatory power, that may shift contention within TTIP negotiations away from investment.

[1] See Jeswald W. Salacuse, “BIT by BIT: The growth of bilateral investment treaties and their impact on foreign investment in developing countries,” The International Lawyer (1990): 655-675; Jeswald W. Salacuse, “The Treatification of International Investment Law,” Law & Business Review of the Americas 13 (2007): 155; Edward Montgomery Graham, Fighting the wrong enemy: Antiglobal activists and multinational enterprises (Washington, DC: Peterson Institute, 2000).

[2] See Deborah L. Swenson, “Why do developing countries sign BITs,” UC Davis Journal of International Law & Policy 12 (2005): 131.

[3] Germany, 203; the United States 114. Source: http://investmentpolicyhub.unctad.org/IIA/IiasByCountry#iiaInnerMenu

[4] Edward Montgomery Graham, Fighting the wrong enemy: Antiglobal activists and multinational enterprises (Washington, DC: Peterson Institute, 2000).

[5] The July 2001 Free Trade Commission Interpretation made minor clarifications in the areas of transparency and the meaning of “fair and equitable treatment,” while being unable to agree on important others, such as “expropriation,” “national treatment.” http://www.iisd.org/pdf/2001/trade_nafta_aug2001.pdf.