INSM via Flickr

A New Fiscal Policy Regime? Germany’s Fiscal Policy in the Wake of the Pandemic

Björn Bremer

Max Planck Institute for the Study of Societies

Björn Bremer is a Senior Researcher in International and Comparative Political Economy at the Max Planck Institute for the Study of Societies in Cologne. He holds a PhD from the European University Institute and his research lies at the intersection of comparative politics, political economy, and political behavior. He is particularly interested in the politics of macroeconomic policies, welfare state politics, and the political consequences of economic crises.

Many observers were surprised by Germany’s fiscal policy response to the Covid-19 pandemic. Not only did the parliament temporarily suspend the constitutional debt brake (Schuldenbremse), but also the government orchestrated a massive fiscal response to combat the economic fallout of the pandemic. It passed several stimulus packages and pushed for a European recovery fund (Next Generation EU) that boosted the EU’s fiscal responses to the crisis.

Following two years of deficit spending in 2020 and 2021, the new coalition government that was elected in September then agreed to increase government debt further. Although it pledged to return to the debt brake in 2023, it proposed additional borrowing for 2022 and set up a special fund (Sondervermögen) worth 60 billion to combat climate change and finance the country’s digitalization. This “Climate and Transformation Fund” draws on unused borrowing that was originally earmarked to combat the Covid-19 pandemic. Its primary purpose is to support Germany’s green transition in the coming years by providing resources outside the government’s regular budget.

Overseen by the FDP finance minister Christian Lindner, this technocratic trick initially surprised many observers. Apparently, however, the use of these special funds has become a pet move of the traffic-light coalition to circumvent Germany’s fiscal rules, as chancellor Olaf Scholz announced another special fund worth 100 billion in February 2022 in order to increase military spending in the wake of the war in Ukraine.

Some pundits, therefore, argue that the pandemic led to a fundamental change in Germany’s fiscal policy regime. Indeed, talk about the country’s beloved “black zero” fiscal deficit (Schwarze Null) is practically obsolete, as the government overcame its debt aversion due to the fallout from the pandemic. Yet, there are some reasons to question whether this amounts to a full paradigm shift.

First, these funds are a technocratic fix that cannot solve a large, structural problem. The one-off accumulation of debt may be a pragmatic way to increase spending in specific areas but Germany’s fiscal rules will still prevent the government from doing so in many others. This could also undermine the success of these very funds, as governments may not be able to hire new staff that are needed to implement many of the planned investment projects. As the debt brake is scheduled to come back into effect in 2023, Germany’s fiscal rules will thus continue to restrain the government in the next few years. As during the interregnum between the 2008 financial crisis and the Covid-19 pandemic, this could result in underinvestment and underutilization of resources.

The use of structural funds to finance much-needed public spending also undermines the democratic accountability of fiscal policy. It forces the parliament to approve an increase in government debt without a clear indication of when and for what purposes this debt will be used. Parliamentary oversight still exists but some of the conventional control mechanisms that allow the parliament and the general public to hold the government accountable are circumvented, thereby making fiscal policy more opaque and threatening its democratic legitimacy.

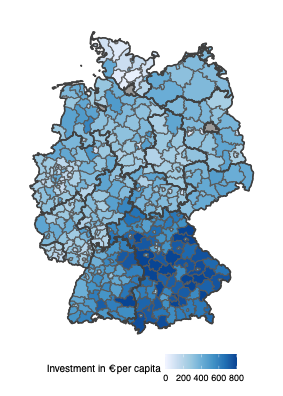

Second, Germany’s state governments are arguably more constrained by the debt brake than the federal government. While the federal government is still allowed to run a small deficit once the debt brake is reinstated, the states are not. This has consequences for state and even local governments, as the latter often rely on financial support from higher levels of government. Combined, these two layers of governments are responsible for implementing the bulk of public spending in Germany, including in crucial areas such as education or infrastructure investment. Although some state governments used the pandemic to set up special funds similar to the federal government, fiscal conditions vary considerably across states. The results are large disparities in the quantity and quality of public services across Germany.

For example, the map below shows the level of local government investment before the pandemic, documenting severe inequalities between different regions which had been increasing for some time. Going forward, the fallout from the pandemic, in combination with the reintroduction of inflexible fiscal rules, is likely to worsen the problem even further. Despite attempts to address this, Germany is not well placed to address the mounting regional inequalities hidden behind the aggregate lack of investment.

Figure 1. Per Capita Public investment of All German Districts in 2018

Source: Bremer, di Carlo and Wansleben (2021)

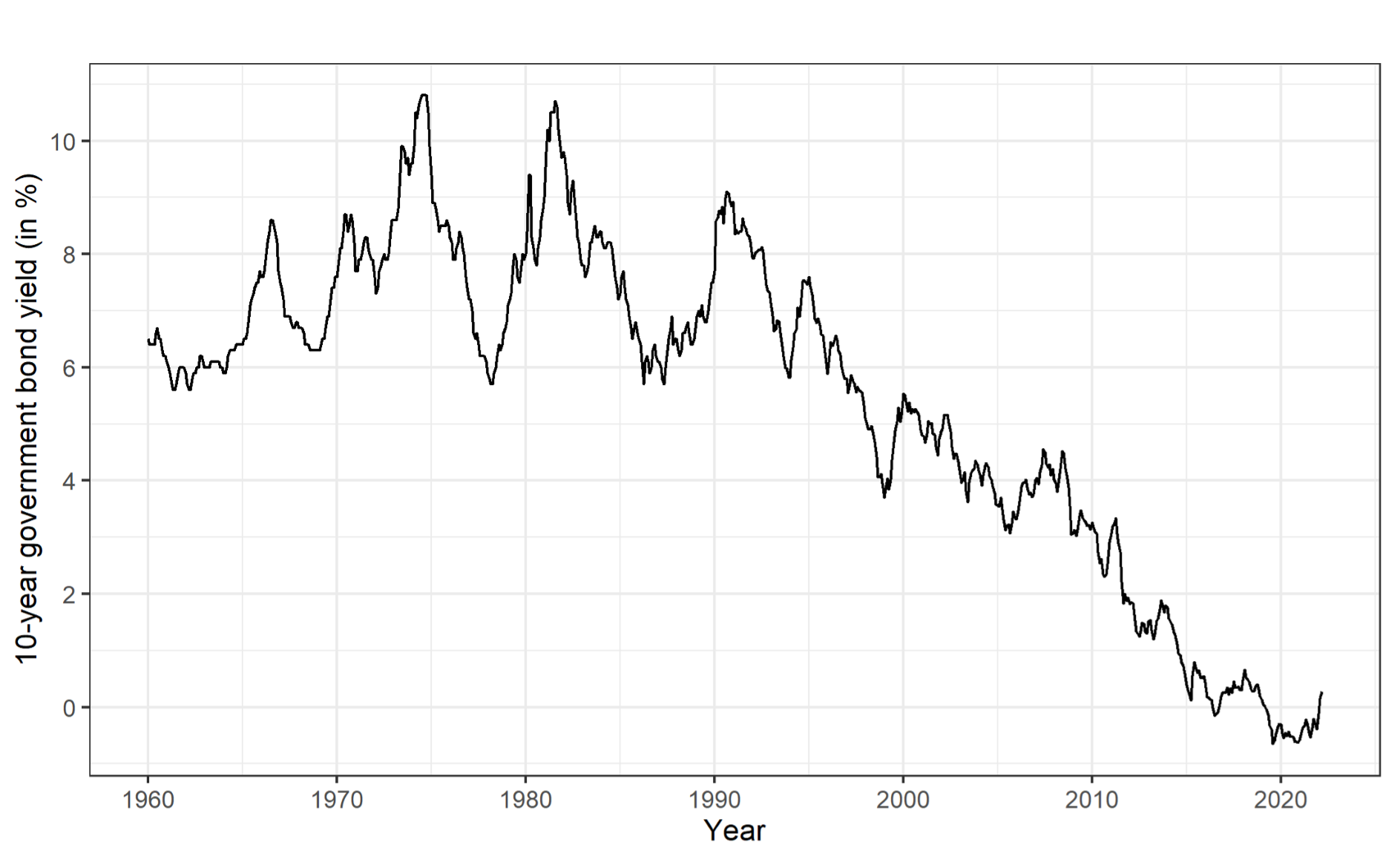

Third, there is room for more expansionary fiscal policies. Although inflation and interest rates are rising, the yield on German government bonds remains extremely low compared to the past, as the figure below shows. The financing costs of German public debt, therefore, are still favorable, which gives the government a lot of room for maneuver. It should use this to boost aggregate demand in the face of a possible economic downturn (e.g., as a result of the Ukrainian war), to prevent continued underinvestment and to address rising economic inequalities.

Figure 2. Yields on 10-Year German Government Bonds from 1960 until 2022

Source: Bundesbank, own illustration

Some may, of course, argue that increased spending becomes less important in the context of rising inflation. However, contrary to received wisdom, there is an argument that governments should spend more rather than less in the current context. As low-income consumers are hit particularly hard by price increases due to broken supply chains and exogenous shocks in energy prices, governments need to cushion the distributive effects via increased government spending. While central banks try to address inflation by raising interest rates and ending quantitative easing, governments need fiscal space for redistributive policies. Otherwise, they risk exacerbating economic grievances and anxieties that fuel contemporary political discontent.

The recent changes in Germany’s fiscal policy regime thus fall short of a paradigm shift. This is also evident in European negotiations about reforms to the Stability and Growth Pact and the governance of the eurozone, where the government remains reluctant to endorse bold action that is necessary to increase Europe’s fiscal space and prevent another lost decade. The fallout from the pandemic, the war in Ukraine, and the enormous costs of the green transition are all good reasons for Germany to truly break free from its constraining pre-pandemic fiscal policy consensus. One can only hope that Olaf Scholz and his government live up to this task.