Why Germany and the U.S. Should Embark on a Large-Scale Investment Program Now

Björn Bremer

Max Planck Institute for the Study of Societies

Björn Bremer is a Senior Researcher in International and Comparative Political Economy at the Max Planck Institute for the Study of Societies in Cologne. He holds a PhD from the European University Institute and his research lies at the intersection of comparative politics, political economy, and political behavior. He is particularly interested in the politics of macroeconomic policies, welfare state politics, and the political consequences of economic crises.

In recent years, fiscal policy in Germany and the U.S. has diverged. In response to the financial crisis both countries implemented large stimulus programs, but over time the policy priorities shifted: German finance ministers became obsessed with balancing the budget, while the Trump administration slashed taxes.

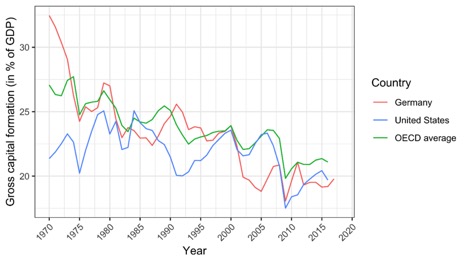

On both sides of the Atlantic, the biggest loser from these development has been investments in physical and human capital. In times of fiscal squeeze, investments are usually abandoned first. Its benefits only materialize in the long term and the support constituency is diffuse. Consequently, gross capital formation as a share of GDP has dramatically declined across advanced economies in the last five decades (Figure 1). The situation is particularly bad in Germany and the U.S. In both countries, there has been an “investment” gap for a long time, and despite some increases in investment in the last few years, the share of investment remains chronically low.

Figure 1: Gross capital formation as a share of GDP in Germany and the U.S., 1970-2018

The results of this shortfall in public and private investment are already dramatic: bridges are collapsing, trains are not running, schools and universities are hemorrhaging, and swimming pools are closing. In the long term, however, the consequences of this under-investment are possibly even more severe. The lack of investment contributes to low productivity, threatens economic competitiveness, and undermines the long-term prospects for economic growth. It also contributes to rising regional inequality and political turmoil, as regions that are left behind fall back even further.

Policymakers in Germany and the U.S. should, therefore, shift their fiscal priorities: they need to develop large-scale investment programs that safeguard economic prosperity. This would not only help to revitalize regions that are left behind, but it would also help to expand the economic potential on both sides of the Atlantic. Unless policymakers act fast, their countries will lose the physical and human capital to compete in the twenty-first century.

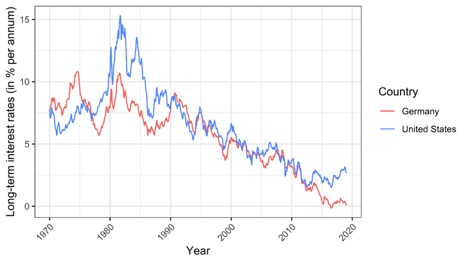

Policymakers are in luck, though: there is no better time to develop a new “Marshall plan” than today. On the one hand, governments in advanced countries can finance debt very cheaply. Interest rates on government bonds remain extremely low (see Figure 2) and, as Olivier Blanchard recently pointed out, this allows governments to issue debt without large fiscal costs. This is particularly true for the Germany: yields on German government bonds have just turned negative, meaning that the government can issue debt of up to ten years at negative interest rates. Private investors would essentially subsidize a public investment program in Germany.

Figure 2: Long-term interest rate on German and U.S. government bonds, 1970-2020

On the other hand, a large investment program today could also be a much-needed fiscal stimulus tomorrow. In the last few years, demand in advanced economies has mostly been supported by monetary policy, but amid the slowing of a global economy, this is not enough. The balance sheets of central banks remain bloated, and as the chances of another recession are increasing, fiscal policy will have to pick up the slack. Yet, fiscal policy, and especially productivity-increasing investments, often have a time lag because it takes time to develop and implement them. Policymakers would thus do well to start spending soon: today’s investments could be the stimulus of tomorrow.

In sum, the current macroeconomic environment presents policymakers with a unique opportunity: as they implement economic policies that are good in the long run, they can also reap benefits in the short run. They would do well not to squander the opportunity.