Globalization: As Bad as Its Reputation?

Jörn Quitzau

Bergos AG

Joern Quitzau is a Geoeconomics Non-Resident Senior Fellow at AGI. He is Chief Economist at Bergos, a private bank based in Switzerland. He specializes in economic trend research and economic policy. Joern Quitzau hosts two Economics podcasts.

Prior to his position at Bergos, Joern Quitzau worked for Berenberg in Hamburg (2007-2024) and Deutsche Bank Research in Frankfurt (2000-2006) with a special focus on tax and fiscal policy.

Dr. Quitzau (PhD, University of Hamburg) was a Visiting Fellow at AGI in April 2014 and September 2022 and an American-German Situation Room Fellow in April 2018.

There are rough times ahead for the ideas of free trade and globalization. U.S. president Donald Trump (who seems to prefer less rather than more economic openness), the Brexit vote, or the anti-TTIP mood in Germany: wherever you look, the rejection of globalization is widespread.

Apparently, many people want more than just a promise that free trade will create growth and prosperity. At first glance, the increasing demands being put on international economic policy are astonishing because globalization has had considerable positive effects over the last two decades. Since 1995, the global economy has grown by a dynamic average annual rate of 3.5 percent. As a result, the financial situation of many people around the world has significantly improved: roughly 1 billion people in developing and emerging countries have managed to escape absolute poverty. Thus, the textbook wisdom that a reduction of trade barriers boosts economic growth has been confirmed in reality. But highly aggregated macroeconomic data can only tell us so much. We need to dig deeper.

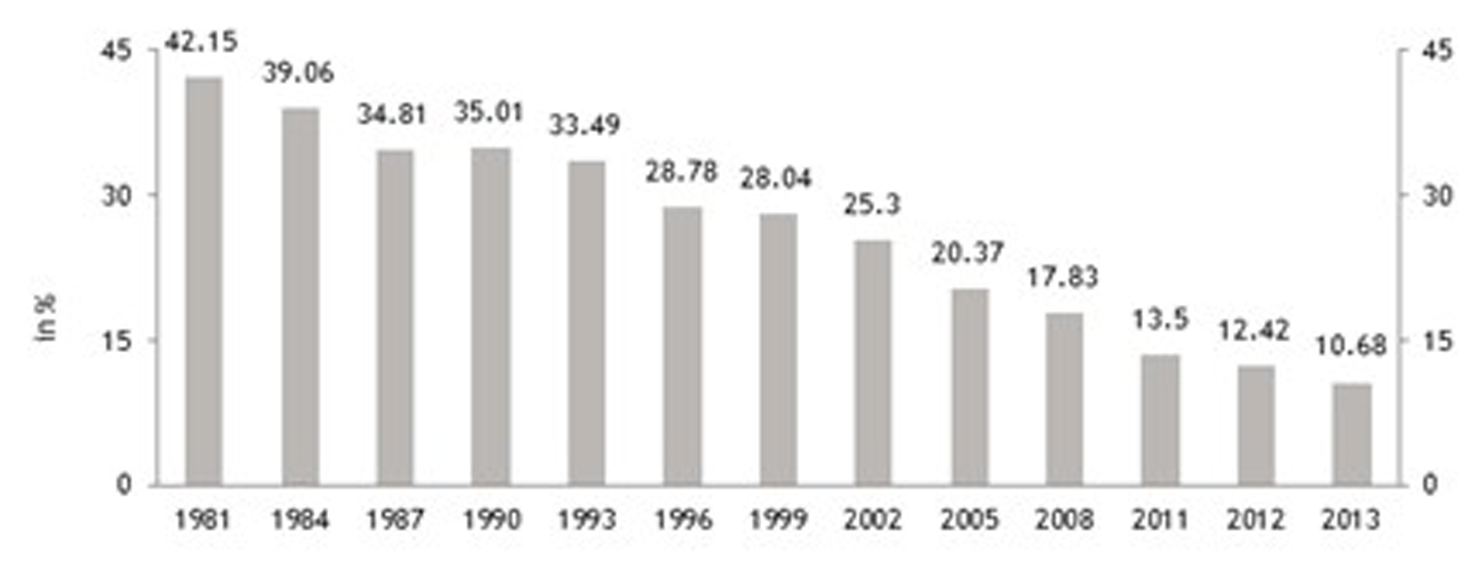

A significant decline of absolute poverty

Source: World Bank. Poverty headcount ratio at $1.90 a day (% of population)

Growing Inequality, But No Polarization of Incomes

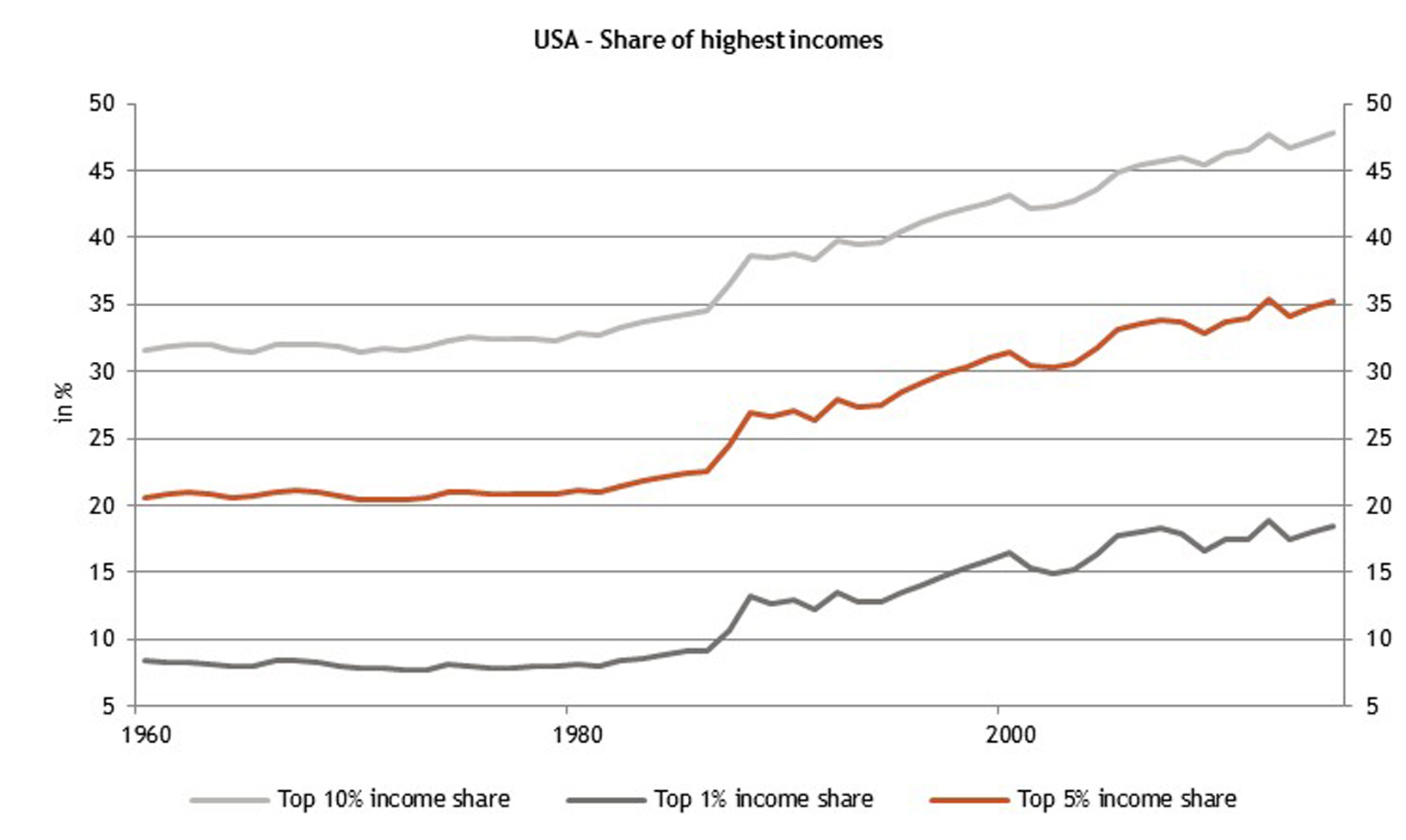

A second glance at the data shows, for example, that in addition to the world’s poorest people, the richest are also cashing in on the advantages of globalization. In the United States, the top 1 percent of the income scale has increased its share from 8 percent of total income in the early 1980s to 18 percent in 2015. In the same period, the top 10 percent has increased its share from 33 percent to 48 percent. The results are less stark in the large, middle-income segment than those at the upper and lower ends of the global income scale show. In many advanced industrial economies the income disparity (measured by the Gini coefficient) initially increased but has flattened out during the last few years. To speak about a polarization of incomes would therefore be too extreme.

However, it is worth mentioning that major parts of the American workforce have been excluded from this generally positive income development. According to the United States Census Bureau, the inflation-adjusted median earnings of male workers have not increased since 1973. To be sure, this has not mainly been caused by the economy’s openness—technological change has been the main cause—but strong international competition has certainly played a part in the increased pressure on incomes and wages.

Share of highest incomes in the U.S.

Source: The World Wealth and Income Database.

Economic Data Doesn’t Paint the Whole Picture

The unease about globalization can be partly explained by the above-mentioned data on income distribution. Economists usually prefer working on economic growth rather than on distribution issues. For economists, an economic policy measure (such as trade liberalization) is beneficial when the resulting gains of one group exceed the losses of another group. That way, the winners can compensate the losers and a net gain remains for the winners—from a theoretical point of view, no one should be dissatisfied. In this academic framework, it does not matter whether losers get compensation in real life or not: the possibility of compensating them is what matters. Understandably, however, most people are not interested in this kind of theoretical perspective. Their concern is first and foremost to improve their own lives. To sharpen the argument: there is no way to win over the losers of globalization by explaining to them that their losses are being outweighed by the gains of people somewhere across the country or—even more so—at the other end of the world. For the general acceptance of globalization, it is crucial that people feel the advantages in their own wallets.

Further challenges lie ahead. Digitization is the next trend that could increase income inequality. The reduction of trade barriers enables companies to supply larger markets. Successful global players increase profits and they are able to pay higher salaries. In combination with technical progress (digital change), markets often follow the winner-takes-all rule with marginal costs hardly playing any role in the digital economy. As a result, companies can stretch out production without incurring additional costs and the winner of the resulting cutthroat competition can achieve something close to a global monopoly. It is no wonder that according to the Forbes list of world’s richest people, the 100 richest people of the technology sector together own $892 billion.

If the positive dynamics of globalization are to be maintained, a certain level of income inequality needs to be accepted: the question is how much, and what can be done about it. IMF director Christine Lagarde recently suggested enlarging the social safety net and supporting further education, both as a way to manage and compensate structural change in a global economy. Lagarde’s ideas point the way forward, but it is important not to underestimate the challenges to implementing them.

First, social security systems are under pressure—in a globalized economy it is easy to switch production to another country when domestic taxes and social security contributions rise. Second, while it is important to help people improve their knowledge and skills, the pace of change in a digitized economy makes it hard to keep up. The most promising avenue is to start investing in people’s education while they are still young and then provide opportunities for life-long learning. Beyond technical skills, part of that process should include a broad-based education that enables people to face challenges and constant change. This strategy, however, only pays off in the long run.

To Manage Globalization, Think and Act Local and Global

In addition to the right domestic policies, better governance and a smarter and more stable regulatory framework are necessary to help face the uncertain world ahead—both at national and international level. A globalized economy needs global institutions that are powerful enough to manage challenges that cross borders. Economic accidents will always happen, and it will be a major political task to contain such accidents and avoid the feeling that the end of the world is nigh, as some may have come to believe in the past few years. To sum up: Where national institutions are unable to sort out local problems, transnational institutions—regional ones like the European Union or global ones like the IMF and the World Bank—are essential.

There is no use in drawing battle lines between the advocates and the critics of globalization and to make a religious war of it. What the world needs is a pragmatic approach. Globalization must be managed in a way that its productive force can unfold without severe distortions. A good plan would be to avoid an all-or-nothing approach. Sometimes more integrated markets and shared sovereignty will be the answer, and sometimes preserving local or national approaches will be important. Slow but steady wins the race.